As Find more information an outcome, individuals may buy policies on unfavorable terms. In reaction to these concerns, many countries have actually enacted in-depth statutory and regulatory routines governing every aspect of the insurance organization, including minimum standards for policies and the ways in which they might be marketed and sold. For instance, most insurance coverage in the English language today have actually been thoroughly drafted in plain English; the industry found out the hard way that numerous courts will not impose policies versus insureds when the judges themselves can not understand what the policies are stating. Normally, courts interpret obscurities in insurance coverage policies versus the insurer and in favor of protection under the policy.

While on the surface it appears the broker represents the purchaser (not the insurer), and usually counsels the purchaser on proper coverage and policy restrictions, in the vast majority of cases a broker's compensation is available in the kind of a commission as a percentage of the insurance coverage premium, creating a dispute of interest in that the broker's monetary interest is slanted towards encouraging a guaranteed to purchase more insurance coverage than may be required at a greater rate. A broker normally holds agreements with lots of insurance companies, thus permitting the broker to "shop" the market for the best rates and coverage possible.

A connected representative, working solely with one insurance provider, represents the insurance coverage business from whom the policyholder purchases (while a complimentary representative sells policies of different insurance companies). Just as there is a potential conflict of interest with a broker, an agent has a various kind of dispute. Since representatives work directly for the insurance coverage company, if there is a claim the agent may recommend the customer to the benefit of the insurance provider. Representatives generally can not provide as broad a variety of choice compared to an insurance coverage broker. An independent insurance specialist advises insureds on a fee-for-service retainer, comparable to a lawyer, and thus provides entirely independent suggestions, devoid of the financial dispute of interest of brokers or representatives.

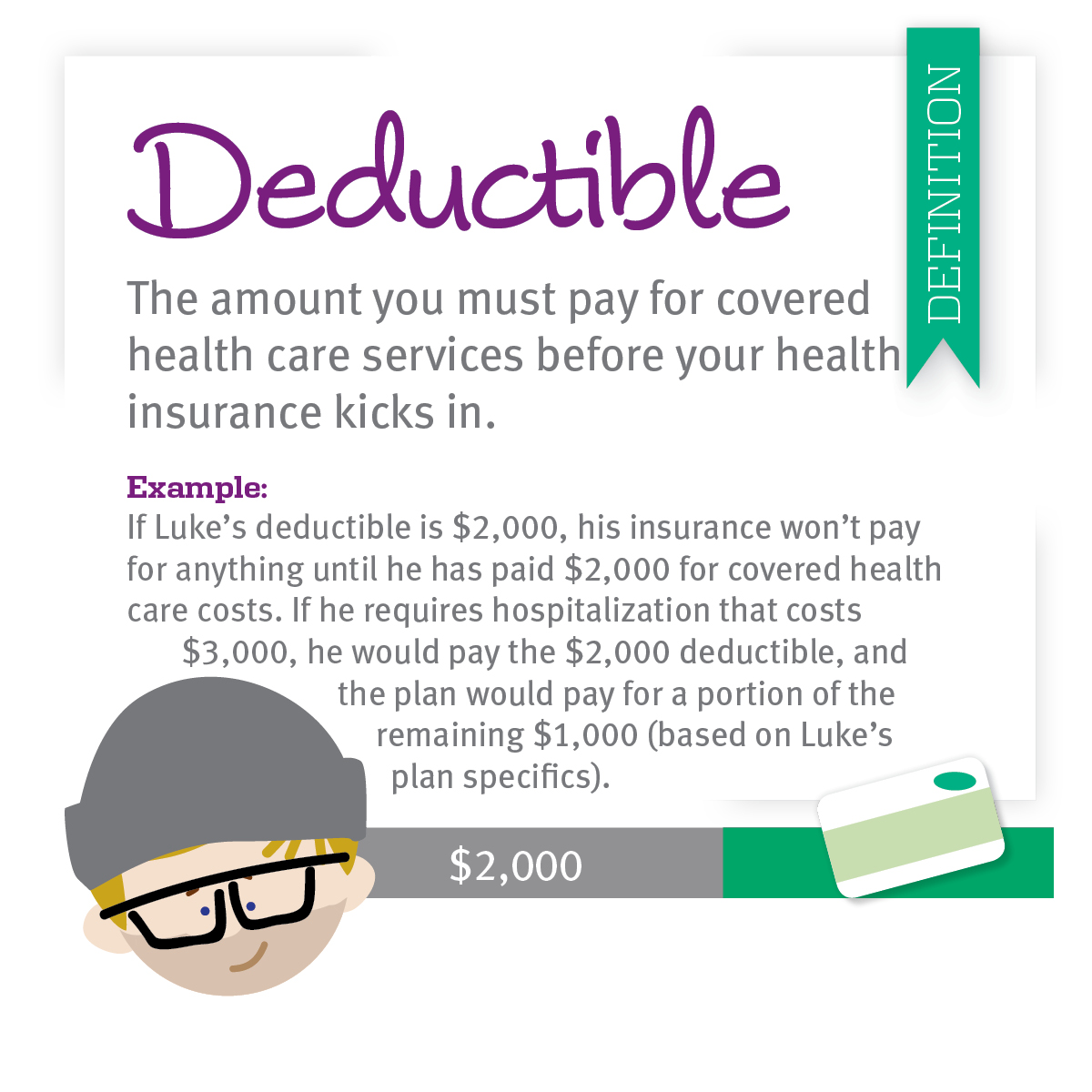

In the United States, financial experts and consumer advocates usually consider insurance to be rewarding for low-probability, catastrophic losses, but not for high-probability, small losses (What is whole life insurance). Because of this, customers are encouraged to select high deductibles and to not guarantee losses which would not trigger a disruption in their life. Nevertheless, customers have shown a tendency to prefer low deductibles and to prefer to insure reasonably high-probability, small losses over low-probability, maybe due to not comprehending or neglecting the low-probability threat. This is related to lowered getting of insurance against low-probability losses, and may lead to increased inefficiencies from moral threat. Redlining is the practice of denying insurance protection in specific geographical locations, apparently due to the fact that of a high probability of loss, while the alleged inspiration is unlawful discrimination.

From an evaluation of industry underwriting and marketing materials, court files, and research by government firms, market and community groups, and academics, it is clear that race has long impacted and continues to impact the policies and practices of the insurance coverage industry. In July 2007, the United States Federal Trade Commission (FTC) launched a report presenting the outcomes of a research study worrying credit-based insurance coverage ratings in vehicle insurance. The study discovered that these ratings are efficient predictors Visit this website of danger. It likewise showed that African-Americans and Hispanics are substantially overrepresented in the most affordable credit history, and substantially underrepresented in the highest, while Caucasians and Asians are more equally spread out throughout ball games.

The FTC indicated little data was offered to evaluate advantage of insurance coverage ratings to consumers. The report was challenged by representatives of the Consumer Federation of America, the National Fair Real Estate Alliance, the National Customer Law Center, and the Center for Economic Justice, for depending on data offered by the insurance market. All states have arrangements in their rate guideline laws or in their fair trade practice acts that forbid unfair discrimination, often called redlining, in setting rates and making insurance available. In figuring out premiums and premium rate structures, insurance providers think about measurable factors, consisting of area, credit scores, gender, occupation, marital status, and education level.

Little Known Facts About What Is Medigap Insurance.

An insurance underwriter's job is to assess a given threat as to the likelihood that a loss will occur. Any element that causes a higher probability of loss must in theory be charged a greater rate. This standard concept of insurance coverage must be followed if insurance coverage companies are to remain solvent. [] Thus, "discrimination" versus (i. e., unfavorable differential treatment of) potential insureds in the risk examination and premium-setting process is a required by-product of the basics of insurance underwriting. [] For circumstances, insurance companies charge older individuals substantially greater premiums than they charge more youthful people for term life insurance coverage. Older people are hence dealt with differently from more youthful individuals (i - What does renters insurance cover.

The rationale for the differential treatment goes to the heart of the risk a life insurance company takes: older people are most likely to die sooner than young people, so the threat of loss (the insured's death) is higher in any given period of time and therefore the threat premium must be higher to cover the greater threat. [] However, treating insureds in a different way when there is no actuarially sound factor for doing so is unlawful discrimination. New guarantee items can now be protected from copying with a service method patent in the United States. A recent example of a new insurance coverage item that is trademarked is Use Based auto insurance coverage.

Many independent creators favor patenting new insurance products given that it provides protection from huge business when they bring their brand-new insurance items to market. Independent developers account for 70% of the new U.S. patent applications in this location. Numerous insurance coverage executives are opposed to patenting insurance products due to the fact that it produces a new risk for them. The Hartford insurance coverage company, for instance, recently needed to pay $80 million to an independent innovator, Bancorp Services, in order to settle a patent infringement and theft of trade secret claim for a type of business owned life insurance item created and patented by Bancorp.

The rate at which patents have been issued has gradually risen from 15 in 2002 to 44 in 2006. The very first insurance coverage patent to be approved was consisting of another example of an application posted was US2009005522 "risk evaluation business". It was posted on 6 March 2009. This patent application describes an approach for increasing the ease of altering https://pbase.com/topics/tirgonmoge/omkdupq444 insurance provider. Insurance coverage on demand (likewise Io, D) is an insurance service that provides clients with insurance coverage defense when they require, i. e. only episodic rather than on 24/7 basis as generally provided by standard insurance companies (e. g. clients can buy an insurance coverage for one single flight instead of a longer-lasting travel insurance plan).